¿Es rentable ser propietario de un banco? Un análisis en profundidad

Owning a bank can be highly profitable. Banks generate income through loans, fees, and investments. Profitability depends on economic conditions, regulations, and costs. This article explores how profitable is owning a bank and what influences these profits.

Principales conclusiones

Bank profitability is primarily derived from net interest margin, service fees, and interchange fees, which collectively contribute to substantial earnings in the American banking sector.

Understanding the cost structure, including operating and infrastructure costs, is essential for analyzing a bank’s financial performance and profitability potential.

Regulatory impacts, such as capital requirements and compliance costs, significantly affect bank profitability and operational strategies, necessitating careful management to maximize returns.

Understanding Bank Profitability

Banks play a crucial role in the financial system by allowing customers to change the timing of their cash flows. Understanding bank profits begins with knowing how banks generate income. Banks profit from several sources: fees, net interest margin, and interchange fees. The American banking market is one of the most profitable globally. Each year, banks in this sector generate profits amounting to hundreds of billions.

Profitability extends beyond making money; it enables banks to build risk buffers, invest in long-term projects, and return value to shareholders. Sustaining future profitability involves having a clear vision, long-term investments, and a robust capital base. This profitability serves as a critical performance indicator for privately owned banks.

Net Interest Margin

The net interest margin, a fundamental metric for bank profitability, is calculated as the difference between the income earned from loans and the interest paid on deposits. Banks profit from this margin by charging higher interest rates on loans than what they pay depositors. Fluctuations in interest rates can significantly impact a bank’s earnings, as changes can alter borrowing costs and loan yields.

Typically, rising interest rates enhance earnings by widening this gap, directly influencing profit margins and financial performance.

Service Fees

Another vital revenue stream for banks is service fees. Banks often impose various fees for account maintenance, transactions, and additional banking services to enhance profitability. From credit card fees to ATM fees, these charges accumulate to form a significant portion of bank account revenue.

Charging fees for services allows banks to cover operating expenses and infrastructure costs, ensuring sustainable financial performance.

Interchange Fees

Interchange fees are another significant source of revenue for banks. These fees are paid by merchants’ banks to consumers’ banks when card transactions occur. This system allows banks to profit from every transaction made using their issued credit or debit cards. By charging these fees, banks can generate substantial income, further contributing to their overall profitability.

Revenue Streams in Banking

Banks are financial institutions that generate income through various means. One primary source of revenue is charging interest on loans, which significantly impacts bank profitability. Additionally, banks derive income from investment activities and gestión de patrimonios services, diversifying their revenue streams.

Fractional reserve banking amplifies profitability by allowing banks to lend a portion of deposits, though it introduces liquidity risks. Wealth management services, including financial advising and investment management, also enhance profitability by attracting clients seeking comprehensive financial services.

Loan Interest

Interest from loans is a primary revenue source for banks, significantly influencing overall profitability. Different types of loans, such as mortgages, personal loans, and auto loans, contribute to this revenue stream. By charging interest on these loans, banks can generate steady income, which is crucial for maintaining a profitable business model.

Investment Income

Banks also generate income through investments in capital markets and securities. By engaging in capital markets and mutual funds, financial institutions can supplement their earnings. This is how banks make money.

Diversifying revenue streams through investments is essential for banks to reduce risk and enhance profitability.

Wealth Management Services

Providing advisory and wealth management services significantly contributes to a bank’s overall profitability. Offering investment advice and portfolio management helps banks attract high-net-worth clients and provide tailored financial solutions.

These services lead to increased fee income and help in optimizing client relationships, ultimately boosting profits.

Cost Structure of Banks

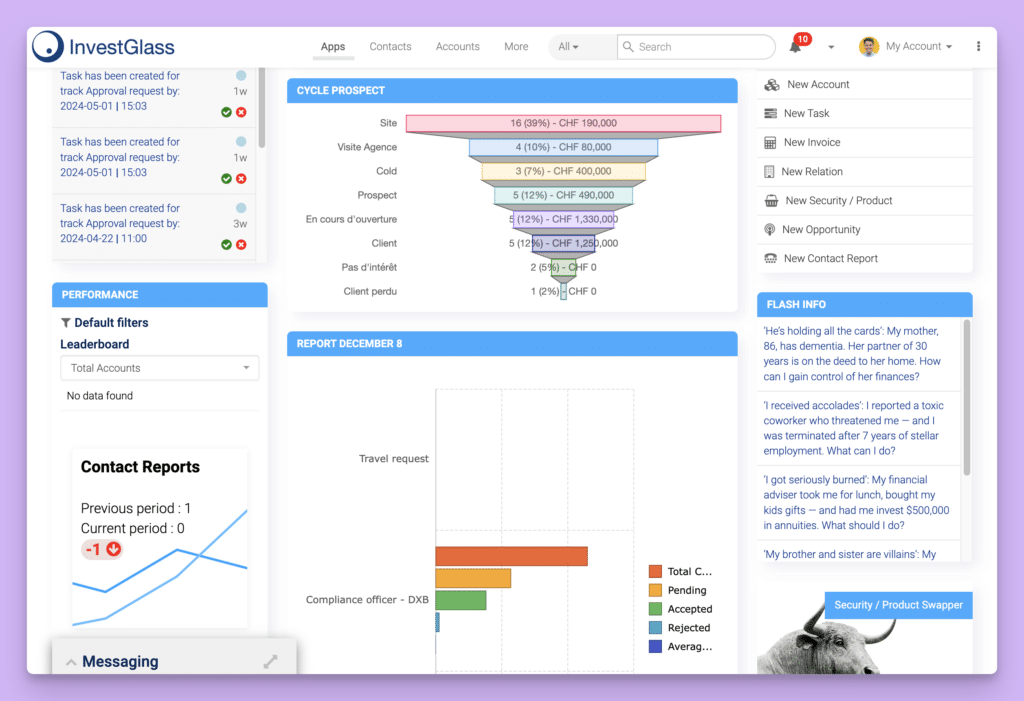

InvestGlass dashbaord

Understanding the cost structure of banks is crucial for analyzing their profitability. Banks incur fixed operating expenses that do not significantly change with the loan amount, making smaller loans less profitable. These expenses are categorized into interest and noninterest costs, with noninterest expenses including operational costs like salaries and technology.

The overall cost structure significantly impacts profitability, especially in relation to operational and infrastructure expenses.

Operating Expenses

Personnel costs typically constitute the largest share of a bank’s operating expenses. Staff compensation, including salaries and benefits, represents a significant percentage of total costs. Additionally, branch maintenance and technology investments are key contributors to operating expenses.

Managing these costs is vital for maintaining profit margins and overall financial performance.

Infrastructure Costs

Maintaining physical branches and digital platforms incurs substantial infrastructure costs for banks. These costs include rent, utilities, and maintenance for physical branches. Setting up a full-service branch can cost approximately $1.5 million, with annual operating expenses reaching around $1 million per branch.

These expenses can significantly impact a bank’s profitability.

Gestión de riesgos

Effective risk management strategies are essential for banks to minimize potential losses associated with credit risk. Managing credit risk and ensuring compliance with regulations involve significant costs that affect overall financial stability. These expenses are crucial for maintaining a healthy capital base and protecting against potential loan defaults.

Regulatory Impact and AI Impact on Profitability

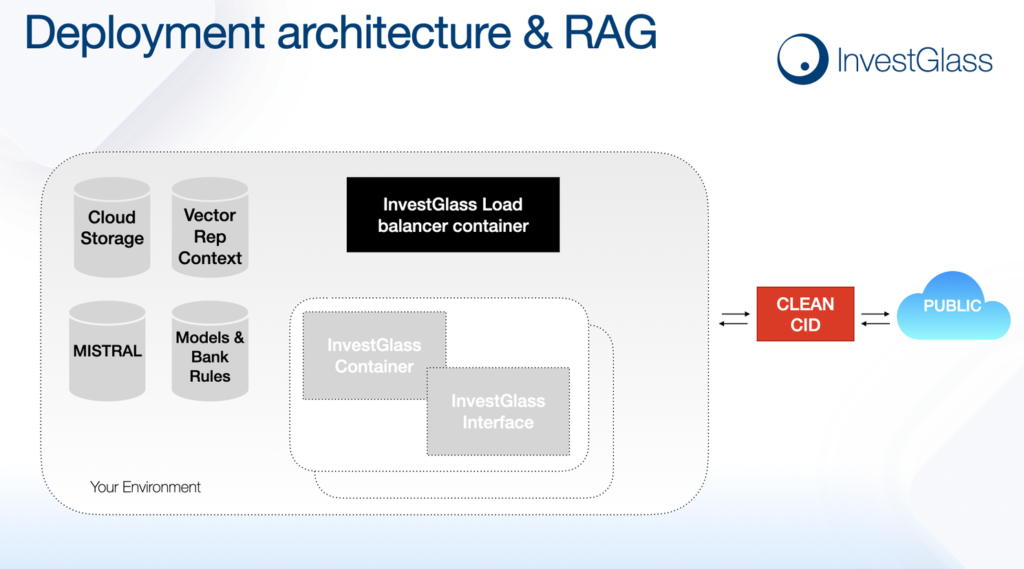

InvestGlass – Get AI Ready

Regulatory requirements have a significant impact on bank profitability. Minimum capital requirements dictate the amount of funds banks must keep on hand, affecting their lending capabilities. Since the global financial crisis, banks are better capitalized and more liquid due to improved regulation and supervision. However, increased regulatory scrutiny can strain profitability by adding compliance and risk management costs.

Owning a bank requires a deep understanding of the financial services industry and a commitment to ongoing regulatory compliance.

Capital Requirements

Regulatory bodies typically impose minimum capital requirements that influence banks’ ability to distribute profits. Starting a bank requires a substantial initial capital outlay, often in the millions, to meet these regulatory and operational needs. Prospective bank owners typically need between $12 million and $20 million for initial capital investment.

Compliance Costs

Meeting regulatory standards often results in significant financial expenses for banks, which can squeeze their profit margins. These compliance costs diminish profit margins and can create operational challenges that necessitate adjustments in bank strategies.

New regulations can impose additional costs and influence bank profitability.

Fractional Reserve Banking

Fractional reserve banking allows banks to lend more than their actual reserves, influencing overall liquidity. This practice can amplify profitability but also introduces liquidity risks.

Understanding the dynamics of fractional reserve banking helps financial institutions manage their funds and maintain profitability while adhering to regulatory requirements.

Large banks leverage extensive resources and strong brand recognition to dominate the market. In contrast, small banks often compete by providing personalized services tailored to individual customer needs. Community banks build strong relationships within their local communities, enhancing customer loyalty.

Online banks have increasingly captured market share by offering lower fees and higher interest rates on deposits and attractive savings accounts.

Economic Factors

Interest rates are pivotal in affecting the profitability of banks. As interest rates rise, banks can earn more from loans compared to what they pay interest to depositors, thereby increasing profitability.

Economic cycles and interest rate changes play a crucial role in determining bank earnings and directly impact their financial performance.

Technological Advancements

Integrating advanced technologies like AI into banking operations is crucial for staying competitive. AI enhances risk management processes by allowing banks to better assess credit risks and manage defaults.

The banking industry is undergoing significant changes due to digital transformation and innovations by fintech companies, reshaping traditional banking models and leading to improved efficiency and service delivery.

Profitability Metrics and Performance Indicators

The profitability of banks can be assessed through various metrics, including net interest margin and service fees. Key profitability metrics for banks include Return on Assets (ROA), Return on Equity (ROE), and the Efficiency Ratio. Banks can achieve nearly 100% gross profits and maintain net margins around 30.89%, making them substantially more profitable compared to many other business types.

Return on Assets (ROA)

Return on Assets (ROA) measures the profit generated per dollar of a bank’s assets, allowing for comparisons across different portfolios. It indicates how effectively a bank utilizes its assets to generate profit, calculated by dividing net income by total assets.

Higher ROA values suggest better performance and more efficient asset utilization.

Return on Equity (ROE)

Return on Equity (ROE) is calculated by dividing net income by shareholders’ equity, serving as an indicator of a bank’s profitability and efficiency. It shows how well a bank generates profit from shareholders’ equity, with higher ratios suggesting better returns for investors.

An average ROE of approximately 14% was reported in late 2021, reflecting a rebounding trend after declines during the pandemic.

Efficiency Ratio

The Efficiency Ratio reflects a bank’s non-interest expenses as a percentage of its revenue, providing insights into its operational efficiency. It is calculated by dividing non-interest expenses by total revenue, with lower ratios indicating better cost management.

Ratios below 50% are considered optimal for bank operations, highlighting effective operational efficiency.

Challenges and Risks in Banking

Regulatory frameworks are designed to enhance the stability of banks, significantly affecting their profit-making strategies. However, these frameworks can also impose constraints that impact profit margins. The potential downside of short-term profit optimization may compromise longer-term resilience and encourage risk-taking.

The global financial crisis exemplified how severe economic downturns can impact bank profitability.

Credit Risk

Credit risk arises when borrowers fail to fulfill their loan obligations, impacting the bank’s financial health. The primary source of credit risk comes from the potential for borrowers to default on loans, leading to significant financial losses for banks.

High levels of borrower default can undermine overall financial stability and profitability.

Interest Rate Risk

Fluctuations in interest rates can influence a bank’s net interest margin, thereby affecting its overall earnings. These fluctuations directly impact profit margins, particularly through net interest income variations. Interest rate changes can disrupt a bank’s earnings and affect its overall financial stability.

Regulatory Changes

Regulatory changes represent a critical factor affecting banks’ operations and overall profitability. Requirements enforced by entities like the Federal Reserve and FDIC directly impact how banks manage their finances and profitability. The costs of complying with regulations impose a significant financial burden, impacting profit margins.

Bank Business Model and Efficiency

A bank’s business model and efficiency play a crucial role in determining its profitability. A well-designed business model can help a bank maximize its revenue and minimize its costs, while operational efficiency enables it to deliver high-quality services to customers at a lower cost. Understanding these elements is essential for anyone looking to delve into the intricacies of bank profitability.

Impact of Different Business Models

Different business models can significantly impact a bank’s profitability. For instance, a bank that focuses on retail banking will have a different approach compared to one that specializes in corporate banking. Retail banks typically have a larger network of branches and ATMs and offer a wide range of consumer banking services, such as credit cards, personal loans, and savings accounts. This model relies heavily on attracting a large customer base and generating income through service fees and net interest margin.

On the other hand, corporate banks may operate with a smaller network of branches but offer specialized services like cash management, financiación comercial, and large-scale loans. These banks focus on building relationships with businesses and generating revenue through higher-value transactions and tailored financial solutions. Each business model has its own set of advantages and challenges, and the choice of model can significantly influence a bank’s profit margins and overall financial performance.

Eficiencia operativa

Operational efficiency is another critical factor in a bank’s profitability. A bank that can deliver high-quality services at a lower cost will naturally be more profitable. There are several strategies banks can employ to enhance their operational efficiency. Investing in technology is one such strategy; by adopting advanced banking software and digital platforms, banks can streamline their processes and reduce manual labor costs.

Additionally, banks can improve efficiency by optimizing their internal processes. This might involve reengineering workflows to eliminate redundancies, automating routine tasks, and implementing best practices in project management. Outsourcing non-core functions, such as IT support or atención al cliente, can also help banks focus on their primary business activities while reducing operational costs.

By focusing on both a robust business model and operational efficiency, banks can enhance their profitability and ensure long-term success in the competitive banking industry.

Emerging Financial Technology Trends

En banking industry is undergoing a significant transformation, driven by emerging financial technology trends. These trends are reshaping how banks operate and creating new opportunities for improving efficiency and profitability. Staying abreast of these developments is crucial for banks aiming to remain competitive and innovative.

Fintech Innovations

Fintech innovations, such as mobile payments and blockchain, are revolutionizing the way banks deliver services to their customers. Mobile payments, for example, allow customers to make transactions using their smartphones, eliminating the need to visit a branch or ATM. This convenience not only enhances customer satisfaction but also reduces the operational costs associated with maintaining physical branches.

Blockchain technology, a distributed ledger system, offers secure and transparent transaction processing. By leveraging blockchain, banks can reduce the risk of fraud, streamline settlement processes, and lower transaction costs. This technology is particularly beneficial for cross-border payments and trade finance, where traditional methods are often slow and expensive.

Inteligencia artificial (AI) and machine learning are also making significant inroads into the banking sector. AI can analyze vast amounts of customer data to provide personalized financial advice and product recommendations, enhancing customer engagement and satisfaction. Machine learning algorithms can detect unusual transaction patterns, helping banks prevent fraud and manage risk more effectively.

Overall, these emerging financial technology trends are creating new avenues for banks to enhance their operational efficiency and profitability. By adopting these innovations, banks can offer better services to their customers, reduce costs, and stay ahead in the rapidly evolving banking industry.

InvestGlass implementation into Credit Agricole Next Bank

InvestGlass, el CRM suizo

Credit Agricole Next Banco

In a strategic move aimed at transforming the customer experience and automating internal operations, Crédit Agricole Next Bank deployed its new prospect management platform and CRM in March 2024. This launch marks a significant step in the digitalisation of retail banking.

Maxime Charton, Deputy Director of Development, is at the forefront of this initiative and expresses his satisfaction with the successful implementation of this new automation tool. “The deployment of InvestGlass within Crédit Agricole’s Next Bank represents much more than a technical improvement; it is a cultural transformation which allows the bank to continue to innovate and improve its digital journeys in the service of its customers”, declares Maxime Charton.

El mensaje adecuado en el momento oportuno, gracias a los viajes personalizados

La elección de InvestGlass como solución de gestión de clientes potenciales responde a un importante reto al que se enfrentaba Crédit Agricole Next Bank: responder eficazmente a las necesidades de una base de clientes en crecimiento gestionando al mismo tiempo una importante diversidad lingüística entre empleados y clientes, que hablan más de cuatro idiomas diferentes. La flexibilidad y las capacidades de automatización de InvestGlass fueron decisivas para ofrecer una respuesta adaptada a este imponente flujo de nuevos clientes, garantizando al mismo tiempo un servicio personalizado y eficaz.

La digitalización de la gestión de prospectos: la plataforma InvestGlass como columna vertebral

The appointment scheduling, prospect flow automation, and mailing tools integrated into InvestGlass were crucial in achieving this objective. They allowed the bank to manage its communications more agilely and personalizedly, regardless of the channel used. “InvestGlass allows us to optimise our operational efficiency while significantly improving our clients’ experience,” adds Stephane Graeffly, Director of the online agency.

Is Owning a Bank Right for You?

Owning a bank can offer significant financial rewards but also comes with substantial risks and responsibilities. Starting a bank is one of the most lucrative business ventures, given the potential for significant profits.

This section helps readers assess if a bank owner is suitable for them.

Financial Commitment

Starting a bank requires a substantial financial outlay for initial capital and ongoing operational expenses. This investment, ranging between $12 million and $20 million, is necessary to meet regulatory and operational needs.

Long-Term Rewards

Owning a bank can yield substantial long-term profits, providing financial security and stability over time. While bank profitable may take years to realize, the potential for steady income through interest on loans and fees makes it an attractive venture.

The long-term profitability of a bank can offer steady revenue and asset appreciation, contributing to overall bank profit.

Personal Suitability

Assessing personal skills, experience, and financial objectives is vital to determine if owning a bank is the right venture. Evaluating qualifications, such as financial expertise and risk tolerance, is necessary before pursuing bank ownership.

Aligning personal financial goals with the demands of bank ownership can help clarify whether this investment is viable.

Resumen

In conclusion, owning a bank can be an incredibly profitable venture if managed well. From understanding various revenue streams and managing costs to navigating regulatory landscapes and competitive dynamics, successful bank ownership requires a blend of financial acumen, strategic planning, and adaptability. By leveraging these insights, potential bank owners can make informed decisions and pave the way for a profitable future in the banking industry.

Preguntas frecuentes

How do banks primarily make money?

Banks primarily generate revenue through interest earned on loans, along with service and interchange fees. This model enables them to sustain and grow their operations effectively.

What is the net interest margin?

The net interest margin is the difference between the income generated from loans and the interest expenses associated with deposits. This key financial measure indicates a bank’s profitability from its lending activities.

What are the significant costs for banks?

Significant costs for banks primarily encompass operating expenses, infrastructure costs, and risk management expenses. These expenses are critical for maintaining efficient operations and ensuring financial stability.

How do regulatory requirements impact bank profitability?

Regulatory requirements affect bank profitability by imposing capital mandates and compliance costs, thereby constraining profit margins. This necessitates a careful balance between maintaining regulatory standards and achieving financial performance.

Is owning a bank a good investment?

Owning a bank can be a lucrative investment opportunity offering substantial long-term profits; however, it necessitates a considerable financial commitment and effective risk management strategies.

Banks play a crucial role in the financial system by allowing customers to change the timing of their cash flows. Understanding bank profits begins with knowing how banks generate income. Banks profit from several sources: fees, net interest margin, and interchange fees. The American banking market is one of the most profitable globally. Each year, banks in this sector generate profits amounting to hundreds of billions.

Profitability extends beyond making money; it enables banks to build risk buffers, invest in long-term projects, and return value to shareholders. Sustaining future profitability involves having a clear vision, long-term investments, and a robust capital base. This profitability serves as a critical performance indicator for privately owned banks.

Banks play a crucial role in the financial system by allowing customers to change the timing of their cash flows. Understanding bank profits begins with knowing how banks generate income. Banks profit from several sources: fees, net interest margin, and interchange fees. The American banking market is one of the most profitable globally. Each year, banks in this sector generate profits amounting to hundreds of billions.

Profitability extends beyond making money; it enables banks to build risk buffers, invest in long-term projects, and return value to shareholders. Sustaining future profitability involves having a clear vision, long-term investments, and a robust capital base. This profitability serves as a critical performance indicator for privately owned banks.

Banks are financial institutions that generate income through various means. One primary source of revenue is charging interest on loans, which significantly impacts bank profitability. Additionally, banks derive income from investment activities and gestión de patrimonios services, diversifying their revenue streams.

Fractional reserve banking amplifies profitability by allowing banks to lend a portion of deposits, though it introduces liquidity risks. Wealth management services, including financial advising and investment management, also enhance profitability by attracting clients seeking comprehensive financial services.

Banks are financial institutions that generate income through various means. One primary source of revenue is charging interest on loans, which significantly impacts bank profitability. Additionally, banks derive income from investment activities and gestión de patrimonios services, diversifying their revenue streams.

Fractional reserve banking amplifies profitability by allowing banks to lend a portion of deposits, though it introduces liquidity risks. Wealth management services, including financial advising and investment management, also enhance profitability by attracting clients seeking comprehensive financial services.