The Banking of the Future: 5 Trends to Follow

The banking industry is evolving rapidly, driven by technological advancements and shifting consumer expectations. By 2025, digital banking will dominate, with over 90% of UK individuals already using online or mobile banking services in 2023 (Compare Banks). The banking industry has been transformed massively by digital transformation. The future of banking is rapidly approaching, and it will be unlike anything we have seen before.

Everything started to change with the advent of customer experience in banking. The banks are now focusing on how their financial services are more user-friendly and attractive to their customers in order to meet their consumer expectations. It is very important to create an atmosphere of trust. This atmosphere of trust can only be built with financial institutions that will generate financial intimacy with your customers. This is what I call the return on consent.

In this blog post, we are going to share five trends that you need to keep an eye on for the future of your bank account and your business! Since 2018 banks are now in a race of cryptocurrency’s. It is not that easy to set up your whole nail bank with existing software’s wealth management of the future will include cryptocurrencies.

1) Digital transformation through your mobile phone

Customer self-service is one of the fastest-growing consumer banking key trends. In many financial institutions, the customer can access financial services from his mobile phone instantly. The mobile application of retail banks became from a nice-to-have to a need-to-have. Another important aspect of mobile banking is that it can generate an additional amount of data for analysis. From customer preferences to numerous financial data, this can be a great source of useful insights to implement in future decisions and strategies and support business growth. When it is done right, investor experience in retail banking leads to more satisfied customers, happier colleagues members, increased process efficiency, accelerated collection of assets, and reduced operational risk!

Mobile phone is the new way to offer financial services. A mobile phone is like real estate. In a crowded city or on a crowded iPhone your investors will be entertained by multiple applications. These applications have to generate financial intimacy and that is not something so easy to do with a digital tool. Investors have to know what is the application about. We suggest an approach that we called super Mario. The super Mario approach means showing new features after the minimum viable journey has been accomplished. Neobanks offering too many services at once will lose their investors’ attention, then trust, and could even generate distrust.

2) Financial services branch of the future

Nowadays, people tend to visit a bank branch only when it is strictly necessary. Neobanks, don’t even have a single physical branch. The digital transformation has allowed customers to perform digital payments online. This does not mean that the physical branch of the bank will remain the same. There is a significant trend toward the rebranding of numerous banks in order to become more user-friendly and up-to-date with the digital trends. This way, most banks will be able to attract more customers and reduce costs.

We believe that the branch of the future should be hosting reach interactions. Offering an opportunity to meet with the team in place that will call the bank will be a true differentiator among all those new neobanks. That’s why starting a neobank is definitely something anyone can do today but building a financial branch it’s another story.

3) Robotic process automation and artificial intelligence

The increased number of customer requests and the inability of banks to fulfill these requests efficiently have created the digital trend of chatbots. Through artificial intelligence, a chatbot can serve customers faster and reduce costs for the bank. On the other hand, through robotic process automation, a bank can improve its onboarding process and take advantage of its sales digital channels more effectively. Furthermore, the bank can eliminate errors since there is better process optimized and effectively secure its customers’ financial data since through task automation there are fewer departments involved.

4) Hyper-personalisation in financial institutions

Online banking is a means to personalize the entire customer journey. Compared to standard personalization, which uses data analytics to deliver targeted products to specific groups, hyper-personalization manages to target each customer individually. Through the use of predictive analytics, AI, and machine learning they can monitor individual customer’s data, like which keywords they usually search, what content they like to view, what is their geographic location, and more. Artificial intelligence is offering a far deeper customer insight than any human. The system is trained with your own data. As each business model are different, we are looking to optimize your key performance indicator. This is how we different banks. Banks will apply the same FINSA or MIFID but the quarterly or investment solicitation produced is completely different.

To remain relevant, traditional banks must be present in the ecosystems and products that customers use. Hyper personalization should restrict to a list of partnerships that will not create too much distraction. Each new partner is an opportunity but can also be a threat! If you are building a mash-up of applications make sure that these applications are interoperable, secured in trusted environments that enable your collaborators and investors to collaborate!

5) Advising services, especially for you

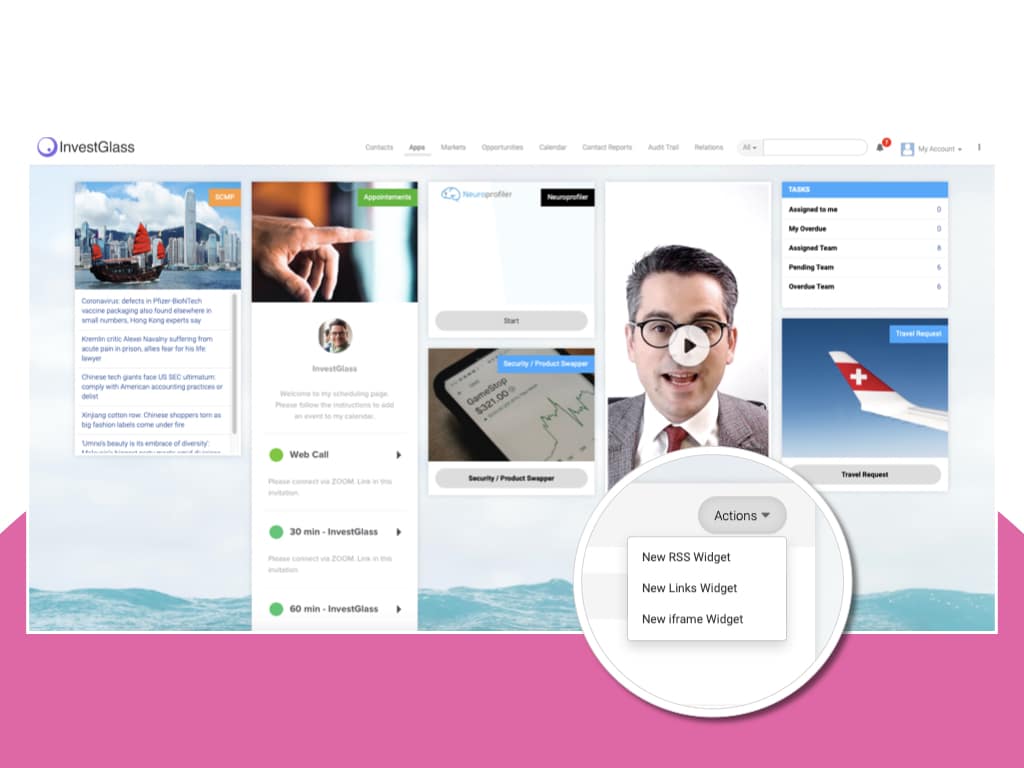

From credit unions to large banking leaders, the main source of profits is advisory services. When it comes to guidance for your portfolio or financial planning for your new house, most customers will never be able to get valuable advice from banks chatbots. With customer relationship management (CRM) technology, you can collect and analyze data and build detailed customer profiles, which your in-house advisors can then use to gain a 360-degree view of the customer and their unique situation. At InvestGlass, we offer a retail banking CRM that digitizes your onboarding and KYC processes, in order to generate more leads and transform the way you sell.

You should set a “Trusted advisor” status. “Trusted advisor” status is what will differentiate banks from all other touchpoints that offer embedded financial services. Investors will trust you not because you are offering the cheapest transaction. The transaction can go as low as to be free, right? But interactions are a completely different value. In a post-Covid World, gaining financial and digital life confidence will be absolutely key to your business growth.

If you’re looking for a digital banking system, we offer tools that will help you get ahead of the banking trends. InvestGlass is a company dedicated to helping banks achieve their goals through digital transformation and customer experience innovation. We create tools, resources, custom solutions, and consulting services designed specifically for bank customers of all sizes. If you’re ready to be ahead of the curve in 2021 when this trend becomes more mainstream, let us know how we can help you today! Our passion with Investglass is to offer embedded financial services by orchestrating fintech together and build an efficient journey.