What Are Banks Doing with ChatGPT?

The integration of artificial intelligence (AI) into the banking industry has significantly transformed customer service, risk management, and overall financial operations. A notable example is JPMorgan Chase, where over 200,000 employeesare actively utilizing AI tools to enhance productivity and customer interactions.

Similarly, BBVA has adopted 3,300 ChatGPT Enterprise licenses, with 80% of employees reporting that ChatGPT saves them more than two hours weekly, improving efficiency across various departments. These developments underscore AI’s pivotal role in revolutionizing the banking sector.

At InvestGlass, we have observed varying behaviors among clients regarding AI adoption. Banks can leverage ChatGPT for enhanced customer support, fraud detection, credit approval processes, personalized wealth management, compliance monitoring, and risk management. By implementing AI strategically, financial institutions can improve efficiency, reduce costs, and enhance customer experiences.

What is the future of ChatGPT in finance?

Harnessing the power of machine learning and natural language processing, ChatGPT has been pivotal in redefining the customer experience. It’s not just about generating human-like responses to user queries or providing accurate customer support. It’s about revolutionizing the way business executives perceive CX (customer experience) and how senior management sufficiently understands the role of digital banking AI. Recent respondents report AI usage that far surpasses half the eurozone average, indicating a swift adoption.

The first test we produced was with open AI chat GPT. Of course, here we have potential risks as the data will go to US-based servers. Lots of our clients were reluctant therefore to use ChatGPT inside the system CRM or PMS. As we are currently adding the solution inside our own premises, the artificial intelligence can be used safely. Financial institutions will appreciate hosting the LLM directly on their servers.

How banks can protect their customer data?

Financial institutions, ever vigilant about risk management, particularly in the realms of anti-money laundering, fraud detection, and identifying potential risk factors, leverage ChatGPT and its underlying technology to monitor user transactions, analyze data, and even identify potential compliance violations. Moreover, with the use of virtual assistants like ChatGPT, banks avoid costly fines by ensuring fewer unsatisfactory customer encounters and ensuring accurate and competent answers. It’s not just about providing security; it’s about streamlining operations and managing potential risks. To leverage generative language tools, we are first fine running the intent with InvestGlass hard-coded rules or via the soft no-code automation tool which banks can customise themselves. Ultimately, only hosting on local server customers’ data.

How will ChatGPT affect banking profitability?

Virtual assistants, as a facet of the wider banking AI scene, enable banking operations to function more efficiently. Routine tasks like account balance inquiries, transaction history checks, and even financial news updates are swiftly handled, freeing customer service representatives to focus on more complex tasks. This not only reduces overhead costs for maintaining large customer support teams but also allows for more personalized customer service, leading to improved users’ financial health.

We believe that monitoring bank transactions will still be hardcoded automation. However, monitoring user transactions, and potential risks can be improved with a machine learning algorithm.

How does robotic process automation affect the finance industry?

According to reports, RPA in banking sector is expected to reach $1.12 billion by 2025. Also, by leveraging AI technology in conjunction with RPA, the banking industry can implement automation in the complex decision-making banking process like fraud detection, and anti-money laundering.

Customer Service Enhancement in Banking Institutions

Financial institutions manage a plethora of queries daily, encompassing topics from account specifics, application statuses, to balance inquiries. The challenge for banks lies in addressing these queries with minimal delays. A Deloitte survey illuminates this challenge: over 80% of customers who utilized chatbots for product-related inquiries in the preceding 12 months expressed an aversion to using them again. Furthermore, 46% voiced a preference for physical branch interactions. Robotic Process Automation (RPA) holds the potential to revolutionize this, automating standardized processes to deliver real-time responses and thus reducing the response time significantly. This not only hastens query resolution but also liberates human resources for more pressing engagements. Augmented by artificial intelligence, RPA is adept at tackling queries necessitating discernment. With Natural Language Processing, Chatbot Automation empowers bots to comprehend and respond in a human-like manner to customer conversations.

Regulatory Compliance in Banking

The pivotal role of banking within the economic framework demands rigorous adherence to multifarious compliance mandates. An Accenture survey from 2016 indicated that a substantial 73% of participants perceived RPA as a transformative tool in the realm of compliance. Operating tirelessly, RPA enhances productivity whilst ensuring impeccable precision, thereby refining the compliance process’s quality.

Accounts Payable & Operational Efficiency

The accounts payable domain within banking is characterized by its repetitiveness. It mandates the extraction, verification, and subsequent processing of vendor information. Robotic Process Automation, supplemented with Optical Character Recognition (OCR) technologies, streamlines this. OCR discerns vendor details from digital or physical forms and supplies this data to the RPA system, which, after verification, processes payments. In case of discrepancies, the RPA system alerts pertinent executives.

Streamlined Credit Card and Mortgage Loan Processing

Historically, credit card application processing was an arduous endeavor, taking weeks to finalize. This protracted timeframe was detrimental both for customer satisfaction and bank expenditures. However, RPA’s introduction has truncated this period to mere hours. Through simultaneous cross-referencing with multiple systems, RPA verifies necessary documentation, conducts background and credit checks, and decides based on established criteria. Similarly, in the U.S., mortgage loan processing averages around 50 to 53 days, navigating through multiple checkpoints. With RPA, this process’s duration can be dramatically shortened, minimizing potential bottlenecks.

Risk Management and Fraud Detection

In this digital era, banks grapple with the omnipresent menace of fraudulent activities. Monitoring every transaction to identify potential malfeasance is an uphill battle. RPA, with its real-time surveillance, identifies and flags anomalous transaction patterns, in some instances even precluding fraudulent activities by implementing preventive measures.

Streamlining the KYC Process & General Ledger Management

The Know Your Customer (KYC) procedure is non-negotiable for banks, typically employing a substantial workforce for customer vetting. Given the enormity of manual processes, many banks have pivoted to RPA for efficient and accurate KYC procedures. Similarly, banks must maintain a meticulous general ledger, a task fraught with potential errors given its reliance on disparate legacy systems. RPA, being technology-agnostic, amalgamates data from varied systems, ensuring accuracy.

Revolutionizing Report Generation, Account Management, and Underwriting with RPA

RPA’s versatility extends to automated report generation, facilitating error-free and swift document creation. In terms of account management, particularly in scenarios necessitating closures, RPA efficiently tracks accounts, automates notifications, and even facilitates closures under certain circumstances. Underwriting, an intricate procedure of evaluating financial transaction risks, has been substantially optimized with RPA, reducing manual errors, biases, and enabling data-driven decisions.

Optimizing Cash Collection, Deposits, and Account Origination

The facets of cash collection and depositing are replete with challenges. RPA, by centralizing records and bolstering transaction security, introduces unprecedented efficiency. The account origination process, traditionally a lengthy procedure, is expedited with RPA, ensuring speedier loan processes and adherence to regulatory stipulations.

In conclusion, the integration of RPA in banking elucidates the potential to augment operations whilst reducing the need for extensive human resources. A survey by PricewaterhouseCoopers in the financial sector underscored this evolution: 30% of respondents were progressively embracing RPA, with many advancing towards enterprise-wide adoption.

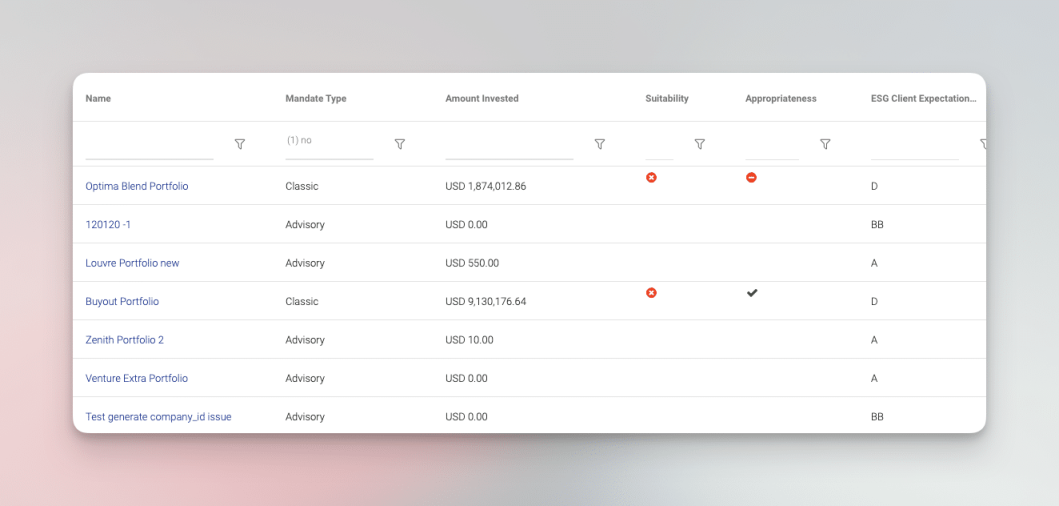

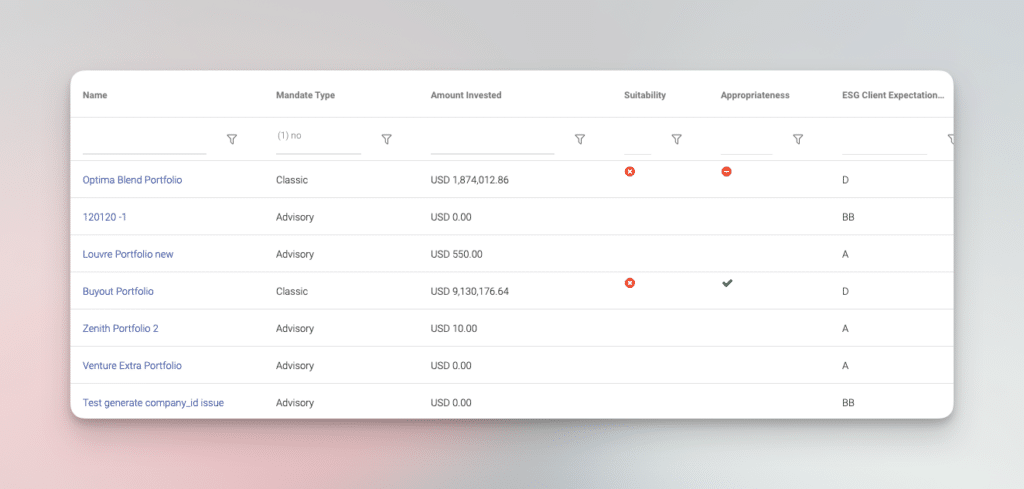

How banks are using InvestGlass to provide personalized financial advice and customer inquiries?

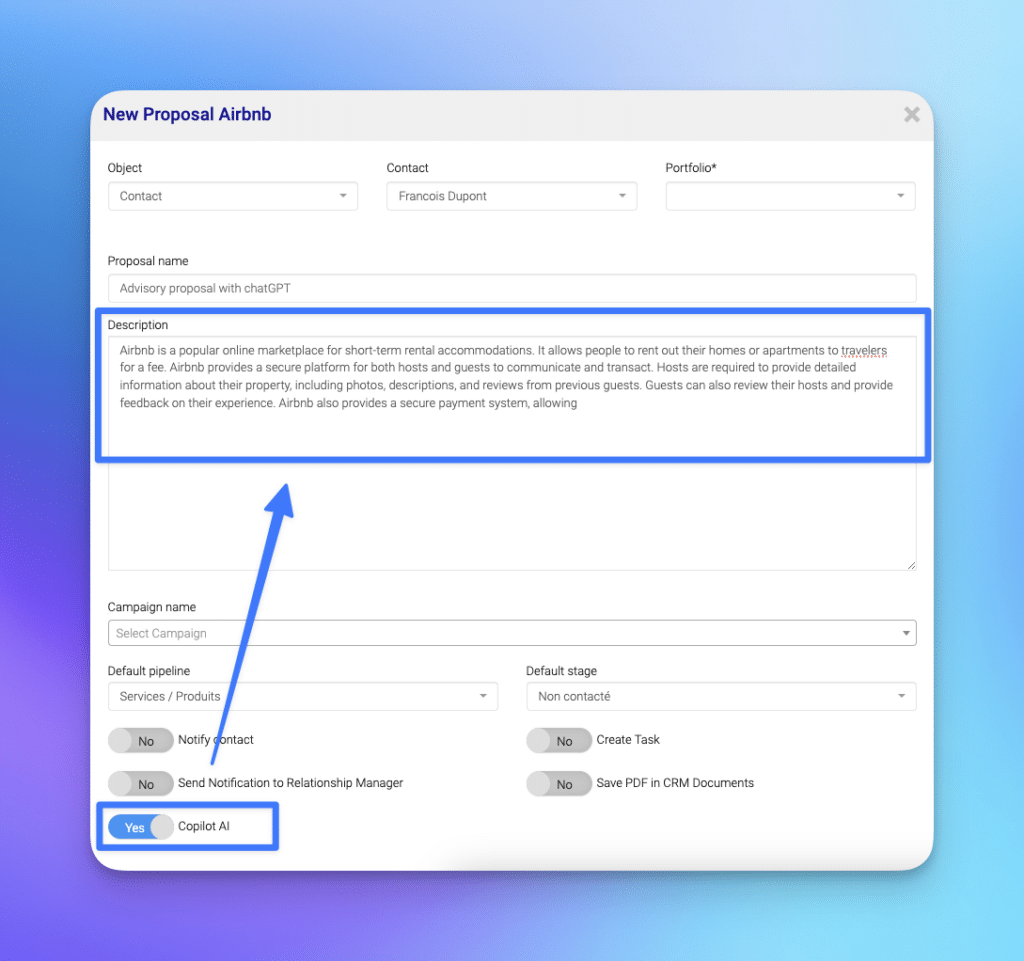

InvestGlass, combined with ChatGPT, is a potent combination for banks to deliver personalized financial advice. AI tools analyze customer data, providing insights into future customer behavior, financial objectives, and even assisting in the development of personalized financial products. By leveraging generative language tools, banks are not only equipped to provide personalized financial advice but can also offer customized financial advice, enabling their customers to make more informed financial decisions.

With this system we can now offer advisory type of service to clients going for discretionary portfolio management. This was incompatible for years as it would have been difficult to analyse customer data without a tool like InvestGlass SA. InvestGlass is blending all data CRM + PMS + KYC + Investment to provide personalized financial advice like never before.

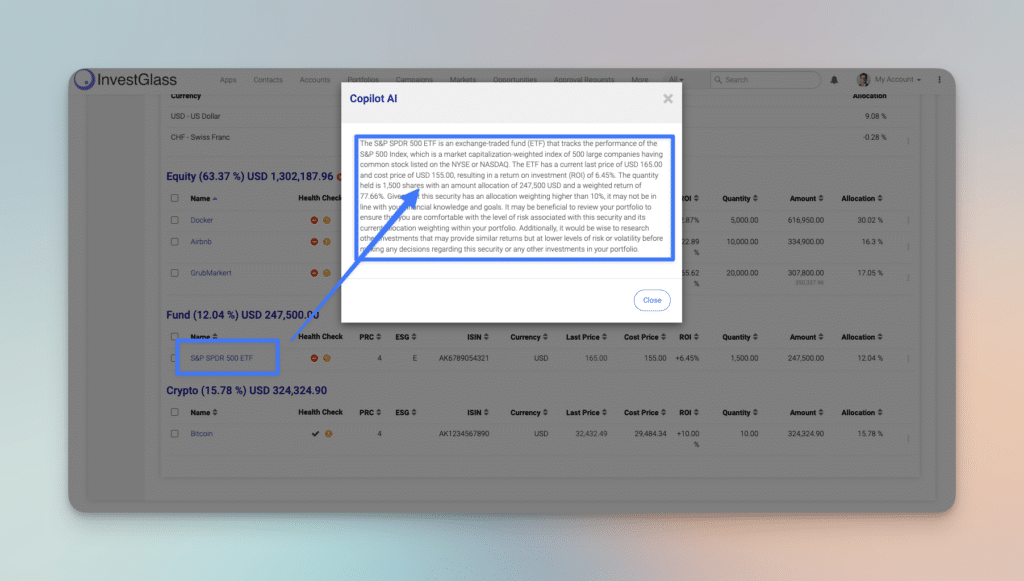

The Automation Revolution with InvestGlass and ChatGPT

InvestGlass, with its advanced automation capabilities, is revolutionizing the banking sector in multifaceted ways. By leveraging generative language tools, it enables banks to provide personalized customer service with unparalleled efficiency. Instead of relying solely on human customer service representatives, the automated customer service, facilitated by InvestGlass, addresses account inquiries banking users may have swiftly and accurately. This ranges from straightforward account balances to more intricate investment advice, thereby enhancing the overall customer experience.

The AI can be used to assist banks or to predict customer service and support. The “whos’s next to be called…how to articulate investment ideas…

Furthermore, InvestGlass assists banks in multiple dimensions. It not only aids in developing personalized financial products tailored to individual user needs but also plays a crucial role in identifying potential compliance violations. With the ever-increasing complexity of global finance, the ability to monitor bank transactions, identify potential fraud, and ensure adherence to regulations through risk management AI is vital. This is especially significant as senior management seeks to sufficiently understand and navigate the maze of regulatory intricacies.

By integrating InvestGlass’s automation, financial advisors can concentrate on the more nuanced aspects of their roles, such as offering personalized wealth management services, rather than mundane tasks. This seamless amalgamation of technology and human touch ensures not only efficient customer service but also strives to improve users’ financial health by addressing customer queries with precision and fostering trust.

In conclusion it will start with customer data

In the ever-evolving landscape of the global financial sector, the integration of advanced technologies such as ChatGPT becomes not just a luxury but a necessity. As banks and financial institutions strive to enhance customer experience, streamline operations, and bolster risk management, leveraging AI tools like ChatGPT proves paramount. Coupled with platforms like InvestGlass, banks now have the unparalleled capability to deliver not just efficient, but also deeply personalized services.

At InvestGlass we believe that global banking sphere will expand with new services, better financial tasks and enhanced future banking user experience. So many financial services that small-size banks will provide with human-like responses and a reduction of potential risk factors.

This is the dawn of a new era in banking, one where AI-driven solutions redefine customer interactions, financial advice, and the very essence of banking operations. As we look to the future, embracing such innovations will undoubtedly be the cornerstone of a successful, modern, and forward-thinking financial institution.